Ⅰ. 현 경제상황에 대한 인식

| □ | 최근 우리 경제는 투자 위축을 중심으로 내수의 증가세가 둔화되는 가운데, 수출이 감소하면서 전반적인 경기가 부진한 모습을 나타내고 있음 |

- 건설업 생산이 감소로 전환된 가운데, 수출 감소 및 교역조건의 악화에 따라 실질구매력을 나타내는 국내총소득의 증가세도 빠르게 둔화되는 추세를 보이고 있음.

| □ | 수요 측면에서는, 투자의 감소세가 지속되고 소비의 증가세도 둔화되는 가운데, 금년 들어 수출도 빠르게 위축되어 전반적으로 총수요가 부진해지는 모습 |

- 설비투자는 반도체산업의 투자 조정에 따른 기저효과에 더하여, 대부분의 제조업에서 가동률이 낮게 유지되는 상황에서 수출 전망도 악화되면서 큰 폭의 감소세를 지속

- 건설투자의 경우에도 토목부문에서 감소세가 유지되는 가운데, 주택 등 건축부문에서도 위축되면서 전반적으로 부진한 상황이 지속되고 있음.

- 민간소비는 정부의 재정사업 등에 긍정적으로 반응하면서 수요 부진을 완충하여 왔으나, 국내총소득 증가율이 하락함에 따라 증가세가 점차 약해지는 모습

- 수출은 글로벌 경제의 성장세가 둔화되는 상황에서, 반도체 경기 호황이 작년 하반기 이후 조정되는 국면에 진입하면서 금년 들어 부진이 심화되고 있음.

| □ | 한편, 장기적 관점에서 볼 때, 최근 국내 경기의 부진한 흐름은 우리 경제가 글로벌 금융위기 이후의 저성장 기조로 다시 점근하는 과정에서 나타나는 현상으로 판단됨. |

- 글로벌 경제의 경우에도, 미국경제의 장기 호황에 의존하여 지난 2~3년간 진행되었던 개선 추세가 종료되고 성장세가 비교적 빠르게 약화되는 모습을 나타내고 있음.

| □ | 이 같은 대내외 경제 여건을 감안할 때, 단기적으로는 대내외 수요 위축에 선제적으로 대응하여 우리 경제의 안정성을 확보하기 위해 재정정책과 통화정책의 조합을 확장적 기조로 운영하는 것이 바람직함. |

- 다만, 단기적 성장률 제고를 정책성과 평가의 지표로 인식하는 태도를 지양함으로써, 경제정책의 효과에 대한 경제주체들의 기대가 지나치게 단기화되는 현상이 확산되지 않도록 관리할 필요

| □ | 보다 중장기적인 시각에서의 경제정책은 생산성 제고를 목표로 하여, 경제주체들의 역량이 최대한 발휘되는 환경을 조성하는 방향으로 설정운용되어야 할 것임. |

- 인구 고령화로 인해 성장의 지속가능성에 대한 우려가 높아지는 상황에서는, 장기적인 생산성 제고를 독려하기 위한 정책의 개발과 실행에 초점을 맞추는 것이 보다 바람직함.

- 경제주체들의 생산성 제고를 위한 노력들이 장기적인 성장잠재력 강화로 연결되기 위해서는, 이에 필수적인 경제사회 환경을 조성하고 유지할 필요가 있음.

- 공정한 시장경쟁 및 법질서 확립을 통해 미래의 경제환경에 대한 불확실성을 최소화하고, 다양한 이해관계자들의 요구에 대해 정부가 합리적인 대응원칙과 일관성을 견지할 필요 - 이러한 경제사회적 환경하에서, 우리 경제의 비효율적 요소들에 대한 개혁을 꾸준히 추진하여, 인적자원과 물적자원의 재배치가 원활히 이루어질 수 있는 시스템을 구축해 나가야 함.

- 또한 형평성과 효율성을 균형적으로 향상시키는 방향으로, 우리 경제의 구조를 개선하는 정책들의 설계와 실행의 속도를 높여갈 필요가 있음.

Ⅱ. 2019~20년 국내경제

1. 대외여건에 대한 주요 전제

| □ | 세계경제는 2019년에 2018년보다 성장세가 둔화된 후, 2020년에는 완만하게 회복되는 것으로 전제 |

- 최근 IMF는 세계경제가 2019년에 미국, 중국, 유럽 등 주요 국가를 중심으로 작년(3.7%)보다 낮은 3.3%의 성장률을 기록하고, 2020년에는 완만한 회복세를 나타낼 것으로 전망함.

| □ | 원유 도입단가는 2019년에 2018년과 유사한 배럴당 70달러를, 2020년에 5% 정도 하락한 66달러 내외를 기록할 것으로 전제 |

| □ | 실질실효환율로 평가한 원화가치는 2019년에 3% 내외 절하된 후, 2020년에는 큰 변동이 없을 것으로 전제 |

2. 2019~20년 국내경제 전망

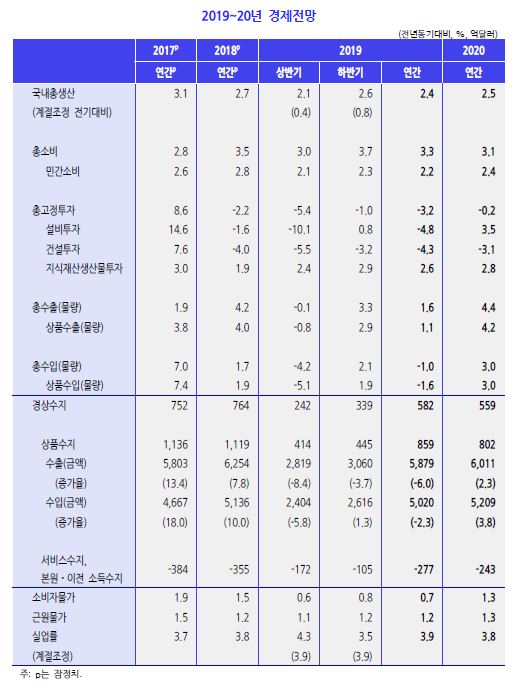

| □ | 우리 경제는 2019년에 내수와 수출이 모두 위축되면서 2.4% 성장한 후, 2020년에는 완만하게 회복되면서 2.5% 내외의 성장률을 기록할 전망 |

- 민간소비는 경제성장률 하락과 교역조건 악화 등으로 실질구매력이 제한되면서 비교적 낮은 증가세를 보일 것으로 예상

- 설비투자는 반도체부문을 중심으로 한 수출 위축에 따라 부진이 심화되고 있으며, 향후에는 세계경기가 개선되면서 점차 회복될 것으로 전망

- 건설투자는 건축부문이 주택건설을 중심으로 감소세를 보이면서 부진이 지속될 것으로 예상

- 수출은 세계경제 성장세 둔화와 수출경쟁력 저하로 당분간 부진한 모습을 보인 후 향후 완만한 회복세를 나타낼 것으로 전망

| □ | 경상수지는 수출 증가세 둔화와 교역조건 악화로 흑자폭이 점차 축소될 것으로 전망 |

| □ | 소비자물가는 공급 측 물가상승 압력이 낮게 유지되고 기대인플레이션이 점차 하락하는 가운데, 우리 경제의 성장세도 둔화됨에 따라 낮은 상승률을 유지할 것으로 예상 |

| □ | 실업률은 경기 부진에도 불구하고 정부 일자리정책 등의 영향으로 2019년(3.9%)과 2020년(3.8%)에 2018년(3.8%)과 유사한 수준을 지속할 것으로 전망 |

- 취업자 수는 2019년과 2020년에 2018년(9.7만명)보다 확대된 20만명 내외와 10만명대 중반 수준의 증가폭을 각각 기록할 것으로 예상

3. 전망의 위험요인

| □ | 대외적으로는 미중 무역분쟁의 심화, 반도체 수요 회복 시기와 정도 등이 우리 경제의 성장세에 작지 않은 영향을 미칠 가능성 |

- 주요 수출대상국인 미국과 중국의 경기가 둔화되고 있는 가운데, 무역분쟁이 원활히 해결되지 못할 경우 우리 경제의 성장세에 부정적 영향을 미칠 가능성

- 2017~18년 중 우리 경제의 성장세를 뒷받침해 온 글로벌 반도체 수요가 2018년 하반기 이후 부진한 모습을 나타내고 있는데, 반도체 수요가 회복되는 시기와 정도에 따라 금년과 내년의 성장률도 전망을 큰 폭으로 상회하거나 하회할 수 있음.

| □ | 대내적으로는 노동시장정책 변경에 따른 단기적 부작용 등이 하방위험으로, 사회안전망 강화 정책의 가시적인 성과 확산은 상방위험으로 작용 |

- 최저임금 인상, 노동시간 단축 등 노동시장정책 변경의 부작용이 나타나면서 성장세가 둔화될 가능성이 존재

- 반면, 기초연금, 근로장려세제 등 사회안전망 강화 정책이 민간소비의 확대로 이어질 경우 우리 경제가 예상보다 개선될 가능성

Ⅲ. 정책방향

1. 재정정책

| □ | 재정정책은 당면한 현안에 대한 추가적인 재정 수요에는 보다 적극적으로 대응하되, 재정건전성에 미치는 영향을 최소화할 수 있도록 세부 지출항목을 면밀하게 검토하여 추경을 편성할 필요 |

- 추경을 위한 추가 국채 발행 계획이 과중한 수준은 아니라고 판단되나, 추경의 특성 및 법적 요건 등을 감안하여 해당 지출이 장기적으로 고착화되지 않도록 관리한다는 원칙하에 세부 항목을 엄격한 기준으로 평가하여 편성할 필요

| □ | 향후 국세수입 증가세가 둔화될 것으로 전망됨에 따라, 강도 높은 지출구조조정을 통해 재정 운용을 효율화하는 등 재정의 지속가능성을 제고하는 노력을 지속할 필요 |

2. 통화정책

| □ | 통화정책은 낮은 물가상승세와 경기 부진이 지속되고 있음을 감안하여 확장적인 기조로 운용하는 가운데, 경제여건 변화에 충분히 신축적으로 대응할 수 있도록 준비할 필요 |

- 최근과 같이 물가상승률이 0%대로 하락하고 대내외 수요가 위축되고 있는 상황에서는 이에 상응한 정도로 충분히 확장적인 통화정책 기조가 필요함.

| □ | 한편, 통화당국은 물가안정목표의 의미와 기준을 명확히 제시하면서 시장과 소통하고, 목표보다 낮은 물가상승률이 장기화됨에 따라 경제주체들의 기대 인플레이션이 낮은 수준으로 고착되는 현상이 발생하지 않도록 유의할 필요 |

- 물가안정목표제의 대상이 되는 ‘물가’에 대해 명확히 설명하고 일관된 운용을 견지함으로써, 통화정책을 포함하여 미래의 경제환경에 대한 경제주체들의 예측 가능성을 높일 필요가 있음.

- 물가상승률이 통화정책의 물가안정목표를 하회하는 상황이 장기화되면서 기대 인플레이션도 낮은 수준에 고착되고 있을 가능성에 유의할 필요

Ⅰ. Current Economic Conditions

| □ | Overall economic activities in the Korean economy have been sluggish as the growth in domestic demand slows on shrinking investment and export growth receded. |

- Production in construction swung to a decrease and the GDI growth, which significantly affects real purchasing power, is sliding fast on falling exports and worsening terms of trade.

| □ | On the demand side, investment continues to decline, consumption growth is slowing and exports are exhibiting a steep contraction from this year, pointing to overall weakness in aggregate demand. |

- Facilities investment remains on a rapid downward trajectory as export prospects, coupled with the base effect from the adjustment in semiconductor investment, deteriorate amid consistently low capacity utilization rates in most manufacturing industries.

- Construction investment remains weak overall as the civil engineering sector continues to descend and the building construction sector shrinks led by housing.

- The positive response in private consumption towards government-financed projects has acted to buffer the sluggish demand, but its growth is gradually slowing on the decrease in GDI growth.

- Amid the slowing growth of the global economy, exports are decelerating further as semiconductors enter an adjustment phase after booming until 2H 2018.

| □ | From a long-term perspective, Korea’s recent economic sluggishness is seen as a phenomenon that stems from the economy gradually approaching to a slow growth trend following the global financial crisis. |

- Growth in the global economy is rapidly weakening as the rebound trend over the past 2-3 years driven by the expansion in the US economy fades.

| □ | Considering the recent changes in internal and external economic conditions, in the short-term, the government should take an expansionary stance in terms fiscal and monetary policies to secure economic stability by preemptively responding to the decline in domestic and overseas demand. |

- However, temporary increases in growth should not become indicators for policy performance to prevent economic agents’ expectations over the policy effects from becoming overly focused on the short-term.

| □ | Rather, policies should be focused on enhancing productivity in the mid- to long-term to create an environment wherein economic agents can fully demonstrate their capabilities. |

- As concerns grow over the effects of population aging on sustainability, policy development and implementation should be aimed at improving long-term productivity.

- In order to bridge the efforts to improve productivity and stronger long-term growth potential, it is important to establish and maintain the necessary social and economic environments.

- The government should work to minimize uncertainties in the economic environment by securing fair market competition and lawful order while holding on to reasonable countermeasures and consistency in response to the various demands of interest groups. - Under such social and economic conditions, consistent efforts must be made to reform the inefficient elements of the Korean economy to build a system that can effectively reallocate human and physical resources.

- Furthermore, efforts must be accelerated to formulate and implement policies that improve Korea’s economic structure in a direction that would enhance equity and efficiency in a balanced manner.

Ⅱ. Domestic Economic Outlook for 2019

1. Assumed External Conditions

| □ | The global economy will grow at a slower pace in 2019 than in 2018 and exhibit a modest recovery in 2020. |

- The IMF forecasts that the global economic growth will slow to 3.3% in 2019 from 3.7% in 2018 led by major countries such as the US, China and Europe, followed by a moderate recovery in 2020.

| □ | Crude oil prices will be similar to 2018 at $70 per barrel in 2019―this will likely recede by 5% to around $66 in 2020. |

| □ | The value of the Korean won, in terms of the real effective exchange rate, will descend by about 3% in 2019 and remain little changed in 2020. |

2. Outlook for Domestic Economy

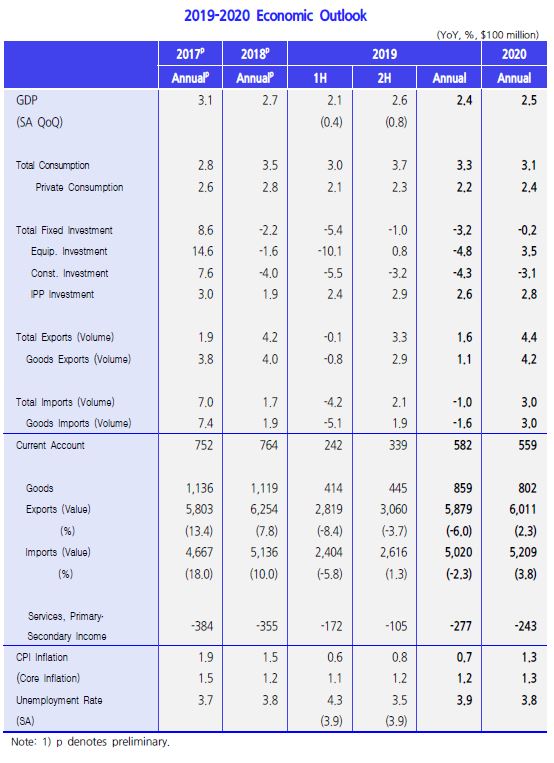

| □ | Korea is forecast to grow 2.4% in 2019 influenced by the decline in both domestic demand and exports and will likely recover at a moderate rate to around 2.5% in 2020. |

- Private consumption will grow at a relatively low rate due to limited real purchasing power on slowing economic growth and worsening terms of trade.

- Led by semiconductors, contracting exports are exacerbating the decline in facilities investment. But, there will be a gradual recovery as the global economy improves.

- Construction investment will stay in a slump as the building construction sector recedes led by housing.

- Exports will be sluggish for the time being due to slowing global growth and weakening export competitiveness, but will likely recover at a modest pace thereafter.

| □ | The current account is projected to run a slightly decreased surplus due to slowing export growth and worsening terms of trade. |

| □ | Headline inflation is expected to remain low as Korea’s economic growth slows amid continued low inflationary pressure on the supply side and gradually decreasing expected inflation. |

| □ | Despite sluggish economic activities, unemployment growth is projected to record 3.9% in 2019 and 3.8% in 2020, similar to the 3.8% in 2018, influenced by the government’s job creation projects. |

- The number of employed persons is expected to record around 200,000 and mid-100,000 in 2019 and 2020, respectively, up from 2018 (97,000).

3. Risks

| □ | Externally, the growing US-China trade disputes and uncertain recovery prospects for semiconductor demand (when and to what degree) could have a considerable impact on the growth of the Korean economy. |

- Amid the slowdown in two of Korea’s major export partners, the trade dispute between the US and China pose a serious threat to the growth of the Korean economy if they remain unresolved.

- The global demand for semiconductors, a key driver of Korea’s economic growth in 2017-2018, started to descend from 2H 2018. The growth rate for this year and next will be largely determined by when and how much the demand recovers.

| □ | Internally, the short-term side effects from the changes in labor market policies could pose downside risks while a spread of tangible outcomes from reinforced social safety net policies will serve as an upside risk. |

- Labor market policies adopted certain changes for minimum-wage increases and shorter working hours, entailing side effects that could weigh on economic growth.

- On the other hand, if the social safety net policies, e.g. basic pension and earned income tax credit, are able to increase private consumption, the Korean economy will improve more than expected.

Ⅲ. Policy Recommendations

1. Fiscal Policy

| □ | Fiscal policies need to actively respond to the additional fiscal demand while detailed lists of expenditure items must be reviewed closely when discussing a supplementary budget to minimize the effect on fiscal soundness. |

- Although the plan to increase government bond issuances to allocate a supplementary budget does not appear excessive, detailed lists of expenditure items must be reviewed and financed strictly based on the principle that the expenditure is not to be permanent, taking into account the characteristics and legal requirements of the supplementary budget.

| □ | Given that the growth in tax revenue is projected to slow, the government should make continuous efforts to improve fiscal sustainabiliy by promoting more efficient management through a strong restructuring of fiscal expenditure. |

2. Monetary Policy

| □ | An expansionary stance should be adopted in terms of monetary policy taking into account the continued low inflation and economic slowdown while making room for flexible responses to changing economic situations. |

- In light of the recent low inflation (0% level) and shrinking domestic and overseas demand, monetary policies need to be expansionary enough to keep pace with the pending situation.

| □ | Meanwhile, the monetary authority should communicate with the markets using explicit definitions of and standards for the inflationary target while taking a cautious approach to prevent economic agents’ expected inflation from being kept at a constantly low level due to the prolonged low inflation. |

- ‘Price,’ as an inflationary target, should be defined clearly and managed consistently in such a way that will enhance the projection ability of economic agents in terms of future economic environments, including monetary policy.

- It should be noted that inflation hovering below the target over an extended period indicates the possibility that the expected inflation could also be stuck at a low level.

제 1 부 경제전망 및 정책방향

Ⅰ. 현 경제상황에 대한 인식

Ⅱ. 2019~20년 국내경제 전망

Ⅲ. 정책방향

제 2 부 경제현안 분석

Ⅰ. 글로벌 금융위기 이후 우리 경제의 성장률 둔화와 장기전망

Ⅱ. 최근 GDP 디플레이터 변동에 대한 분석과 시사점

제 3 부 국내외 경제동향

Ⅰ. 국내경제 동향

Ⅱ. 세계경제 동향

요약

현 경제상황에 대한 인식

2019~20년 국내경제 전망

정책방향

글로벌 금융위기 이후 우리 경제의 성장률 둔화와 장기전망

자세히보기최근 GDP 디플레이터 변동에 대한 분석과 시사점

자세히보기국내경제 동향

세계경제 동향

경제 현안 분석

-

최근 GDP 디플레이터 변동에 대한 분석과 시사점

최근 GDP 디플레이터 변동에 대한 분석과 시사점■ 최근 GDP 디플레이터는 국제유가 등 수출입 가격에 크게 영향을 받은 것으로 나타났으며, 금년 GDP 디플레이터 상승률은 작년에 이어 비교적 낮은 수준에 그칠 가능성이 높을 것으로 전망됨. ■ 금년 GDP 디플레이터 상승률이 낮게 유지됨에 따라 발생할 수 있는 부정적 영향에 대비하는 한편, GDP 디플레이터 상승률의 장기적인 추세가 지나치게 낮은 수준으로 축소되지 않도록 대처할 필요

-

정규철 선임연구위원

프로필

프로필

-

-

글로벌 금융위기 이후 우리 경제의 성장률 둔화와 장기전망

글로벌 금융위기 이후 우리 경제의 성장률 둔화와 장기전망■ 우리 경제는 2011~18년 기간에 연평균 3% 수준의 경제성장률을 기록하였는데, 이는 일시적인 침체라기보다는 추세적인 하락일 가능성이 높은 것으로 판단됨. ■ 성장회계 방법을 연장하여 전망해본 결과, 2020년대 경제성장률은 지속적인 혁신을 통한 생산성 향상을 전제할 경우 연평균 2%대 초중반 수준으로 전망 ■ 이에 따라 생산성 향상을 독려하기 위한 정책적인 노력과 경제성장률 둔화의 원인에 대한 지속적인 모니터링이 요구됨.

-

권규호 연구위원

프로필

프로필

-

한국개발연구원의 본 저작물은 “공공누리 제1유형 : 출처표시” 조건에 따라 이용할 수 있습니다. 저작권정책 참조

무단등록 및 수집 방지를 위해 아래 보안문자를 입력해 주세요.

담당자 정보를 확인해 주세요. 044-550-5454

소중한 의견 감사드립니다.

잠시 후 다시 시도해주세요.