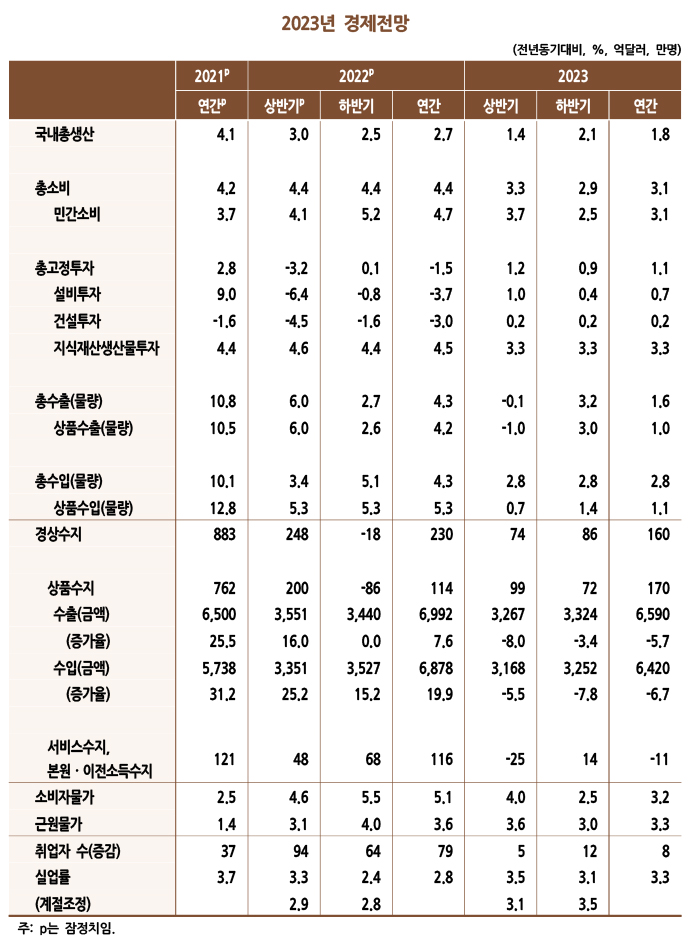

우리 경제는 2023년에 수출 증가세가 크게 둔화되고 투자 부진도 지속되면서 1.8%의 낮은 성장률을 기록할 전망

- 민간소비는 실질구매력 저하와 시장금리 상승으로 재화소비가 둔화됨에 따라 2022년(4.7%)보다 낮은 3.1%의 증가율을 기록할 것으로 전망

- 설비투자는 반도체 경기둔화와 대외 불확실성 증가로 2022년(-3.7%)에 이어 2023년에도 0.7%의 낮은 증가율에 머무를 전망

- 건설투자는 주택시장 부진과 자금조달 여건 악화로 인해 2022년(-3.0%)에 이어 2023년(0.2%)에도 부진이 지속될 것으로 예상

- 수출은 국가 간 인적 이동이 확대되며 서비스수출이 회복됨에도 불구하고, 글로벌 경기둔화로 상품수출이 부진한 흐름을 보이며 1.6% 증가하는 데 그칠 전망

Ⅰ. 현 경제상황에 대한 인식

| □ | 최근 우리 경제는 내수 개선에도 불구하고 대외여건의 악화에 따른 수출 부진으로 성장세가 약해지는 모습 |

- 3/4분기 계절조정 국내총생산(GDP)은 순수출의 성장기여도가 하락하면서 전기대비 0.3% 증가하는 데 그침.

| □ | 내수는 민간소비가 높은 증가세를 유지하고 투자 부진이 일부 완화되었으며, 고용시장도 서비스업을 중심으로 양호한 모습을 유지한 반면, 수출은 글로벌 경기둔화로 부진한 모습을 보이고 있으며, 향후 대외여건이 더욱 악화될 가능성이 높음. |

- 민간소비가 대면서비스업을 중심으로 회복되었으며, 투자도 일시적으로 부진이 완화됨.

- 취업자 수가 큰 폭으로 증가한 가운데, 고용률은 높은 수준을, 실업률은 낮은 수준을 각각 지속하며 양호한 고용시장을 나타냄.

- 그러나 글로벌 경기둔화로 수출금액이 반도체를 중심으로 감소한 가운데, 경상수지는 적자로 전환됨.

- 한편, 소비자물가는 높은 상승세를 지속하고 있으며, 기대인플레이션도 상승함.

- 민간부채가 높은 상황에서 시장금리가 상승하며 내수 회복을 제약하고 있음.

| □ | 대내외 경제 여건을 종합적으로 볼 때, 우리 경제는 수출과 투자의 부진으로 경기둔화 국면에 진입할 것으로 예상됨. |

- 높은 인플레이션에 대응한 주요국의 금리인상과 이에 따른 글로벌 경기둔화로 인해 수출은 부진이 심화될 것으로 예상되며, 코로나 감염병의 영향에서 벗어나면서 대면서비스업을 중심으로 회복되는 민간소비가 경기둔화를 일부 완화할 것으로 전망됨.

- 2023년 우리 경제는 글로벌 경기 부진과 시장금리 상승으로 경기둔화 국면에 머무를 것으로 전망됨.

| □ | 단기적으로는 높은 물가상승세를 감안하여 거시정책을 긴축적으로 운영하는 가운데, 금융건전성을 강화하는 노력도 지속할 필요 |

- 높은 물가상승세가 장기화되고 있어, 기대인플레이션이 물가안정목표 수준에서 벗어나지 않도록 기준금리를 점진적으로 인상하고, 재정지출 증가세도 제어할 필요

- 다만, 향후 경기둔화가 예상되는 점을 감안하여 거시정책 긴축의 속도와 강도를 조절할 필요

- 대내외 금융시장 불안 가능성을 감안하여 거시건전성정책을 정상화하는 기조를 유지할 필요

| □ | 우리 경제는 급속한 고령화로 인해 성장세가 약화되고 있어, 노동공급 축소를 완화하고 생산성을 개선하는 정책적 노력이 요구됨. |

- 인구구조 변화에 주로 기인하여 노동공급이 축소되고 자본축적도 둔화됨에 따라 잠재성장률이 점차 하락할 것으로 전망됨.

- 높은 생산성에도 불구하고 출산과 육아 부담으로 경제활동 참가가 저조한 여성과 급증하고 있는 고령층이 노동시장에 활발히 참여할 수 있는 여건을 마련하고, 외국인력을 적극 수용함으로써 노동공급 축소를 완화할 필요

- 아울러 대외 개방, 규제 합리화 등 우리 경제의 역동성을 강화하기 위한 제도개혁을 통해 생산성을 향상하는 정책적 노력을 경주할 필요

- 한편, 우리 경제의 성장잠재력을 강화하는 노력은 필요하나, 단기적인 경기부양 정책을 통해 잠재성장률을 크게 상회하는 목표를 추구하는 것은 지양할 필요

Ⅱ. 2023년 국내경제 전망

1. 대외여건에 대한 주요 전제

| □ | 세계경제는 2023년에 성장세가 둔화될 것으로 전제 |

- 최근 IMF는 2023년 세계경제가 주요국의 통화긴축 기조 강화와 중국의 경기침체 가능성으로 2.7%의 낮은 성장률에 그칠 것으로 전망함.

| □ | 원유 도입단가(두바이유 기준)는 2023년에 2022년(98달러)보다 15% 정도 하락한 배럴당 84달러 내외를 기록할 것으로 전제 |

| □ | 실질실효환율로 평가한 원화가치는 2023년에 4% 정도 절하될 것으로 전제 |

2. 2023년 국내경제 전망

| □ | 우리 경제는 2023년에 수출 증가세가 크게 둔화되고 투자 부진도 지속되면서 1.8%의 낮은 성장률을 기록할 전망 |

- 2023년 우리 경제는 2% 내외로 추정되는 잠재성장률을 하회하는 성장세를 보이며 경기둔화 국면에 머무를 것으로 전망됨.

- 민간소비는 코로나19의 영향에서 점차 벗어나며 서비스소비가 회복되겠으나, 고물가로 인한 실질구매력 저하와 시장금리 상승으로 재화소비가 둔화됨에 따라 2022년(4.7%)보다 낮은 3.1%의 증가율을 기록할 것으로 전망됨.

- 설비투자는 반도체 경기둔화와 대외 불확실성 증가로 2022년(-3.7%)에 이어 2023년에도 0.7%의 낮은 증가율에 머무를 전망

- 건설투자는 주택시장 부진과 자금조달 여건 악화로 인해 2022년(-3.0%)에 이어 2023년(0.2%)에도 부진이 지속될 것으로 예상됨.

- 수출은 국가 간 인적 이동이 확대되며 서비스수출이 회복됨에도 불구하고, 글로벌 경기둔화로 상품수출이 부진한 흐름을 보이며 1.6% 증가하는 데 그칠 전망

| □ | 경상수지는 2023년에 서비스수지 적자폭이 확대됨에 따라 올해(230억달러)보다 흑자폭이 축소된 160억달러 흑자를 기록할 전망 |

| □ | 소비자물가는 2023년에 국제유가가 안정되면서 상승폭은 축소되겠으나, 여전히 물가안정목표(2%)를 상회하는 3.2%의 높은 상승률을 나타낼 전망 |

| □ | 취업자 수는 2023년에도 양호한 고용 여건이 유지되겠으나 기저효과와 고령화로 인해 2022년(79만명)보다 크게 축소된 8만명 증가할 전망 |

3. 전망의 위험요인

| □ | 미국 금리인상 가속화가 지속되거나 글로벌 경기가 크게 위축될 경우, 우리 경제의 성장세도 수출과 제조업을 중심으로 더욱 둔화될 가능성 |

- 미국의 기준금리 인상이 가속화되며 달러화 강세 현상이 지속될 경우, 여타 국가의 물가상승 압력이 확대되고 글로벌 교역이 위축되면서 우리 수출도 작지 않은 부정적 영향을 받을 가능성

- 중국경기가 제로코로나 정책과 부동산시장 위축 등으로 급락할 경우, 중국 수요 부진으로 우리 수출이 둔화될 수 있으며, 중국의 생산 차질이 글로벌 공급망 교란으로 이어지면서 하방 위험이 크게 확대될 수 있음.

- 이와 함께 우크라이나 사태가 악화되면서 원자재와 곡물가격이 급등할 경우, 전 세계적으로 인플레이션 상승 압력과 경기둔화 압력이 가중될 가능성

| □ | 대내적으로는 기준금리가 가파르게 인상되거나 금융시장에 신용경색이 발생할 경우, 경기둔화가 심화될 수 있음. |

- 민간부채가 높은 상황에서 금리상승은 경기에 작지 않은 하방요인으로 작용함.

- 회사채 시장을 중심으로 기업 자금조달에 차질이 발생하고 확산될 경우, 투자를 중심으로 성장세가 더욱 둔화될 가능성

Ⅲ. 정책방향

1. 재정정책

| □ | 2023년 예산안은 금년도에 비해 재정건전성이 강조된 것으로 평가됨. |

- 총지출 증가율(5.2%)이 총수입 증가율(13.1%)을 하회하면서 GDP 대비 재정수지 적자와 국가채무는 금년 본예산보다 축소될 것으로 계획됨.

- 세부 항목별로는 통화당국의 물가안정을 중시하는 정책 기조에 공조하여, 경기부양보다 경제구조 전환과 취약계층 지원 등에 집중한 것으로 평가됨.

| □ | 중기재정계획에서 코로나19 위기의 급증한 지출을 조정하고 재정건전성을 강조한 것은 바람직해 보이며, 재정의 지속가능성 제고를 위한 효율적 재정운용 방안을 마련할 필요 |

- 2022~26년 국가재정운용계획에서 코로나19 대응을 위해 확대했던 재정지출을 관리하여 중기적으로 국가채무비율을 50% 내외로 유지할 것으로 계획됨.

- 저출산·고령화 등 인구구조 변화에 따라 재정구조를 신축적으로 조정하여 재정여력을 확보하고 재정의 지속가능성을 제고할 필요

2. 통화정책

| □ | 통화정책은 기대인플레이션이 불안정해지지 않도록 당분간 기준금리 인상 기조를 유지하되, 경기둔화 가능성도 함께 고려하여 금리인상 속도를 결정할 필요 |

- 작년 4/4분기부터 물가상승률이 물가안정목표(2%)를 큰 폭으로 상회하고 있어 통화정책 대응이 요구됨.

- 다만, 통화정책을 미래지향적으로 운영한다는 관점에서 향후 경기가 지나치게 위축될 가능성을 감안하여 기준금리를 완만한 속도로 인상할 필요

| □ | 한편, 우리나라의 통화정책은 국내 물가와 경기 여건을 중심으로 운영할 필요 |

- 최근 미국과 유로존에서 정책금리를 가파르게 인상하고 있으나, 우리 경제의 여건을 감안하면 그와 같은 빠른 속도의 금리인상이 요구되지 않음.

- 자유변동환율제도의 취지에 부합하게 환율 변동을 용인하고 물가, 경기, 금융시스템 등 국내 거시경제 안정을 중심으로 통화정책을 수행할 필요

- 아울러 통화당국은 외화자금시장이 불안정해질 경우, 외화유동성 경색과 그에 따른 금융시스템 위험에 대처할 필요

3. 금융정책

| □ | 거시건전성 강화 기조를 유지하는 가운데, 시스템리스크 관리가 부실 누적으로 이어지지 않도록 유의하며 사전적 관리체계도 재점검할 필요 |

- 은행의 기업대출은 지속적으로 증가하고 있으나, 채권시장에서는 자금 공급이 빠르게 감소하여 일시적인 경색이 발생하는 등 금융시장이 불안정한 모습을 나타냄.

- 금융시장 불안 위험이 높을수록 부실 자산을 정리하면서 금융건전성을 강화하는 노력이 요구됨.

- 따라서 일부 자산의 부실이 시스템리스크로 전이될 가능성이 높을 경우에 한하여, 신용경색을 완화하는 정책개입이 필요함.

- 한편, 금융기관별로 시스템리스크에 대한 중요성을 파악하고, 해당 금융기관에 이에 준하는 수준의 건전성 관리 방안을 마련할 필요

| □ | 금리 급등에 따른 취약가구와 영세자영업자의 차환 위험에 대비하여 법정최고금리를 탄력적으로 운용하고, 경기둔화에 대비하여 취약차주 보호 방안을 마련할 필요 |

- 조달금리 상승에도 불구하고 법정최고금리가 고정되어 있을 경우 취약가구는 차환이 제약될 수 있어, 취약가구를 보호하기 위한 제도가 오히려 부담으로 작용할 수 있음.

- 법정최고금리를 시장금리와 연동함으로써 취약계층의 금융시장 접근성을 제고할 필요

- 한편, 향후 경기둔화 시기에 영세자영업자에 대한 보증 수요가 증가할 수 있으므로, 보증기관의 대차대조표 건전성을 선제적으로 강화할 필요

Ⅰ. Current Economic Conditions

| □ |

Despite improving domestic demand, the Korean economy is losing growth momentum as exports turn weak on unfavorable external conditions. |

- The seasonally adjusted GDP increased at a mere 0.3% (QoQ) in Q3, reflecting the declining contribution of net exports to GDP growth.

| □ |

Domestically, the trend of strong private consumption continues, and investment has gathered some steam. The labor market remained resilient owing to the service industry, while exports have slackened on the slowing global economy. External conditions are most likely to exacerbate in the coming quarters. |

- Private consumption rebounded, led by the face-to-face service industry, and the contraction in investment has temporarily eased.

- With a huge gain in the number of employed persons, the employment rate maintained high growth, with unemployment kept low, which indicates strength in the labor market.

- However, the current account turned into a deficit while exports (value) shrank mainly in semiconductors due to the global economic slowdown.

- While headline inflation is rising fast, expected inflation picked up, too.

- The market interest rates moved higher amid rising private debt, putting a drag on the recovery of domestic demand.

| □ |

Given the overall external and internal economic conditions, the Korean economy is heading into a downturn due to lower exports and investment. |

- Exports are expected to weaken further in the subsequent quarters as major countries move toward faster rate hikes to curb high inflation, taking a toll on the world economy. On the other hand, the recovery in private consumption led by face-to-face services will likely help partially offset the economic slowdown as it gradually shakes off the impact of the COVID-19 pandemic.

- In 2023, the Korean economy is expected to remain on a downward slope, reflecting the global economic slowdown and rising market interest rates.

| □ |

In the short term, macroeconomic policy needs to remain tight, given persistently high inflation, while sustaining efforts to improve financial soundness. |

- Considering prolonged higher inflation, it is necessary to gradually raise the policy rate and control fiscal expenditure growth to manage inflation expectations within the target range.

- The pace and timing of macroeconomic tightening need careful calibration in light of the expected economic slowdown.

- The stance of normalizing macroprudential policy should be maintained, considering the risk of potential instability in both domestic and global financial markets.

| □ |

Tackling the economic slowdown contributed by the rapid aging of the population requires policy efforts to moderate the contraction in labor supply and improve productivity. |

- Korea’s potential growth is expected to gradually diminish as the labor supply shrinks and capital accumulation slows, largely due to shifting demographics.

- Employment conditions should be improved to encourage the active participation of women who, despite high productivity, typically stay out of the labor force due to childbirth and rearing, as well as elderly citizens whose proportion is rapidly increasing. Also, a reduction in labor supply needs to be countered by actively accepting foreign workers.

- Concerted policy efforts are also required to achieve higher productivity by completing institutional reforms, such as trade openness and regulatory rationalization, which aim to strengthen Korea’s economic vibrancy.

- While efforts to strengthen the growth potential are of reasonable necessity, the government should not be myopic and focus only on short-term stimulus in seeking a goal that greatly exceeds its growth potential.

Ⅱ. Domestic Economic Outlook for 2023

1. Assumptions on Internal and External Conditions

| □ |

The global economy is assumed to slow down in 2023. |

- The IMF projected that the global economy would record a mere 2.7% due to tighter monetary stances in major economies and the possibility of an economic recession in China.

| □ |

Crude oil prices (Dubai) are assumed to mark around $84 per barrel in 2023, down 15% from 2022 ($98 per barrel). |

| □ |

The Korean won, in terms of the real effective exchange rate, is assumed to depreciate by about 4% in 2023. |

2. Domestic Economic Outlook for 2023

| □ |

The Korean economy is projected to grow by a mere 1.8% in 2023 due to a considerable loss in export growth and a steady decline in investment. |

- In 2023, the Korean economy is likely to remain on a recessionary course, growing slower than its potential rate of 2%.

- Consumer spending is expected to rebound as the pandemic’s impact wears off. Still, private consumption will likely decrease by 3.1% in 2023 from 4.7% in 2022, as real purchasing power weakens on high inflation and goods consumption decreases on increasing market interest rates.

- Equipment investment is expected to remain low at 0.7% in 2023, following the trend of 2022 (-3.7%) on a slowdown in the semiconductor industry and mounting external uncertainties.

- The contraction in construction investment (-3.0% in 2022) is expected to continue into 2023 (0.2%) as the housing market turns weak and financing conditions deteriorate.

- Despite the recovery in services exports backed by increasing human mobility between countries, exports are expected to increase by only 1.6% as goods exports remain stagnant due to the global economic slowdown.

| □ | The current account surplus is projected to decrease to $16.0 billion in 2023 from 2022 ($23.0 billion) as the deficit in the service account widens. |

| □ | With stabilizing oil prices, headline inflation is projected to ease to 3.2% in 2023, but still well above the target (2%). |

| □ | In 2023, employment conditions will remain resilient, but the number of employed persons is expected to increase by about 80,000, a sharp drop from 2022 (790,000) due to the base effect and population aging. |

3. Risks

| □ |

If the US accelerates its rate hikes or the global economy tumbles, the Korean economy will likely see a further contraction, particularly in exports and manufacturing. |

- If the strong dollar persists with faster rate hikes in the US, other countries may face further inflationary pressure with shrinking global trade, which can negatively impact Korea’s exports.

- If the Chinese economy plummets on its zero-COVID policy and property slump, the demand fall in China can cause a decline in Korea’s exports. Also, the production disruptions in China may lead to more disruptions in global supply chains, adding to downside risks.

- Not only that, if raw material and grain prices soar as a consequence of the deepening crisis in Ukraine, the pressures of rising inflation and the economic slowdown will rise significantly worldwide.

| □ |

Internally, if the base rate rises sharply or a credit crunch occurs in the financial market, the Korean economy is likely to see a further contraction. |

- While private debt is high, raising the base rate creates significant downside risks to economic activity.

- In case of corporate financing troubles led by the corporate bond market and if they spill over into other sectors, Korea’s economic growth might fall quite sharply, mainly in investment.

Ⅲ. Policy Recommendations

1. Fiscal Policy

| □ |

The 2023 budget bill puts a heavier emphasis on achieving fiscal soundness compared to this year’s stance. |

- The government’s total tax revenue growth (13.1%) exceeded expenditure growth (5.2%). Hence, the fiscal deficit and government debt as a percentage of GDP is set to decrease from the 2022 main budget.

- In line with the monetary authority’s high priority on price stability, the budget bill focuses on the economy’s structural transformation and support for the vulnerable instead of stimulus programs.

| □ |

The medium-term fiscal management plan adjusted the COVID-19-related additional expenditures as part of the effort to strengthen fiscal soundness, and this may be a step in the right direction. An efficient fiscal management plan is required to achieve stronger fiscal sustainability. |

- The 2023 budget bill aims to manage the government debt ratio within 50% in the medium term by revising the previously set spending increase under the 2022-26 fiscal management plan in response to the COVID-19 crisis.

- The government needs to create sufficient fiscal space and improve fiscal sustainability by flexible management of the fiscal structure in response to changing demographics, such as low fertility and population aging.

2. Monetary Policy

| □ |

The monetary policy needs to remain contractionary for the time being to keep inflation expectations stable while allowing for the possibility of economic slowdown when determining the pace of future rate increases. |

- The inflation rate has been well above the target (2%) since Q4 2021, and bringing it down requires a significant monetary-policy response.

- Still, the forward-looking monetary policy recommends slowly raising the policy rate, given the possibility of severe contraction in economic activity.

| □ |

At the same time, the monetary policy needs to pay particular attention to domestic inflation and economic conditions. |

- A rapid rate hike adopted in the US and Eurozone should not necessarily be the case for Korea considering its current domestic economic conditions.

- It is recommended that the monetary policy should focus on the stabilization of macroeconomic fundamentals, such as inflation, economic activity, and financial system while tolerating currency fluctuations in line with the purpose of the free-floating exchange rate system.

- In addition, if the FX market becomes unstable, the monetary authority should take needed actions to resolve a foreign currency liquidity crunch and resulting risks to the financial system.

3. Financial Policy

| □ |

While maintaining the stance for stronger macro-prudentiality, the government should also reexamine the protocols for ex-ante risk management to prevent a series of insolvency. |

- Banks' business loans continue to grow, but the bond market is experiencing a temporary liquidity crunch, indicative of instability in the financial market.

- The higher the risk of instability in the financial market, the more efforts are required to strengthen financial soundness in parallel with clearing out insolvent assets.

- Accordingly, it calls for effective policy intervention to alleviate the credit crunch only when the risks from a few defaulted assets may transfer to the entire system.

- Meanwhile, the government needs to identify the systemic risks in each financial institution and lay out a soundness management plan that corresponds to their status.

| □ |

The policy needs to manage the legal maximum interest rate in a more flexible manner, considering that soaring interest rates will likely make loan refinancing more difficult for vulnerable households and small self-employed workers. Furthermore, policy programs for vulnerable borrowers are needed to protect them in case of an economic slowdown. |

- Under the fixed statutory interest rate ceiling, vulnerable households may have difficulties refinancing their loan despite rising funding rates. In this sense, the statutory ceiling adopted to protect vulnerable households may pose an obstacle to them.

- It is necessary to enhance the vulnerable’s access to the financial market by linking the legal maximum interest rate with the market interest rate.

- Also, since the demand for credit guarantees for small business owners may increase during an economic downturn, preemptive policy actions are required to strengthen the soundness of the balance sheet of the guarantee institutions.

제 1 부 경제전망 및 정책방향

Ⅰ. 현 경제상황에 대한 인식

Ⅱ. 2023년 국내경제 전망

1. 대외여건에 대한 주요 전제

2. 2023년 국내경제 전망

3. 전망의 위험요인

Ⅲ. 정책방향

1. 재정정책

2. 통화정책

3. 금융정책

제 2 부 경제현안 분석

Ⅰ. 환율 변동이 수출입과 무역수지에 미치는 영향

Ⅱ. 최근 취업자 수 증가세에 대한 평가 및 향후 전망

Ⅲ. 장기경제성장률 전망과 시사점

제 3 부 국내외 경제동향

Ⅰ. 국내경제 동향

1. 국내총생산

2. 경 기

3. 소 비

4. 설비투자

5. 건설투자

6. 지식재산생산물투자

7. 수출입 및 국제수지

8. 노동시장

9. 물 가

10. 금융시장

11. 재 정

Ⅱ. 세계경제 동향

1. 개 괄

2. 주요 국가별 경제상황

3. 환율 및 금리

4. 원자재 가격

요약

현 경제상황에 대한 인식

2023년 국내경제 전망

정책방향

환율 변동이 수출입과 무역수지에 미치는 영향

자세히보기최근 취업자 수 증가세에 대한 평가 및 향후 전망

자세히보기장기경제성장률 전망과 시사점

자세히보기국내경제 동향

세계경제 동향

경제 현안 분석

-

장기경제성장률 전망과 시사점

장기경제성장률 전망과 시사점■ 우리 경제는 글로벌 금융위기 이후 생산성 개선세가 둔화된 데 주로 기인하여 경제성장률이 하락한 것으로 분석됨. - 2001~10년 중에는 자본공급 증가세 둔화에 주로 기인하여 경제성장률이 하락함. - 한편, 1991~2019년 중 노동공급의 성장기여도는 비교적 일정하게 유지됨. ■ 2020년대 이후 인구감소와 급속한 고령화 등 인구구조 변화로 우리 경제의 성장세는 점차 둔화되고, 2050년에는 경제성장률이 0.5% 수준으로 하락할 것으로 전망됨. - 1인당 GDP 증가율은 급속한 고령화로 인해 생산연령인구가 감소하는 반면 경제활동 참가가 적은 고령인구의 비중 증가로 2050년에 1.3% 수준을 보일 것으로 전망 - 이러한 장기경제성장률 전망은 생산성 증가율이 2011~19년의 낮은 수준(0.7%)에서 일부 반등하여 1%를 유지하는 것을 전제로 함. - 한편, 향후 5년간(2023~27년) 우리 경제의 잠재성장률은 2.0% 정도로 전망됨. ■ 우리 경제의 구조개혁을 적극 추진하며 생산성을 개선함으로써 인구구조 변화의 부정적 영향을 완화할 필요 - 대외 개방, 규제합리화 등 우리 경제의 역동성을 강화하기 위한 제도개혁을 통해 생산성을 향상하는 정책적 노력을 경주할 필요 - 높은 생산성에도 불구하고 출산과 육아 부담으로 경제활동 참가가 저조한 여성과 급증하는 고령층이 노동시장에 활발히 참여할 수 있는 여건을 마련하고, 외국인력을 적극 수용함으로써 노동공급 축소를 완화할 필요 - 이와 함께 교육개혁을 통한 인적자본의 질적 역량을 강화하는 노력도 지속할 필요 ■ 한편, 거시정책 기조 설정에도 장기경제성장률의 하락 추세를 반영할 필요 - 우리 경제의 성장잠재력을 강화하는 노력은 필요하나, 단기적인 경기부양 정책을 통해 잠재성장률을 크게 상회하는 목표를 추구하는 것은 지양할 필요

-

김지연 전망총괄

프로필

프로필

-

정규철 선임연구위원

프로필

프로필

-

KDI허진욱

-

-

최근 취업자 수 증가세에 대한 평가 및 향후 전망

최근 취업자 수 증가세에 대한 평가 및 향후 전망■ 최근의 이례적인 고용 호조세는 코로나19 위기에 대응하고 적응하는 과정에서 비대면?디지털경제와 관련된 노동 수요가 증가한 데 주로 기인한 것으로 판단됨. - 코로나19 위기는 대면서비스업 고용에 큰 충격을 준 반면, 비대면 경제와 4차 산업으로의 전환을 가속화시키면서 관련 분야의 고용이 확대됨. ■ 2023년에도 양호한 고용여건은 이어지겠으나, 인구구조 변화가 취업자 수 감소의 요인으로 전환되고 기저효과가 작용하면서 취업자 수 증가폭은 2022년(79.1만명)보다 크게 축소된 8.4만명으로 전망됨. - 내년 취업자 수는 기저효과의 영향으로 인해 증가폭이 크게 축소되겠으나, 고용여건 변화에 의한 취업자 증감을 주로 반영하는 고용률 변화의 기여도는 약 10.2만명으로 양호한 수준을 유지할 것으로 예상됨. - 다만, 생산가능인구와 인구구성비 등 인구구조의 변화는 취업자 수 감소(-1.8만명) 요인으로 전환되며, 인구구조 변화의 노동공급에 대한 부정적 영향이 가시화될 전망 - 핵심노동인구 비중이 지속적으로 감소하고, 15세 이상 생산가능인구도 향후 감소세로 전환될 것으로 예상됨에 따라, 인구구조의 변화는 향후 취업자 수 둔화의 주요 요인으로 작용할 전망 ■ 노동투입의 감소는 우리 경제의 성장률 하락으로 이어질 수 있는바, 노동공급을 확대하기 위한 정책적 노력이 필요함. - 여성, 젊은 고령층, 외국인 등 현재 충분히 활용되고 있지 않은 인력풀의 활용도를 높이는 한편, 장기적으로는 출산율 제고를 위한 노력도 기울일 필요 - 이러한 노동공급의 양적인 개선과 함께, 노동생산성을 향상시키고 빠르게 변화하는 노동 수요에 신속하게 대응할 수 있는 인력양성 시스템을 구축할 필요

-

김지연 전망총괄

프로필

-

-

환율 변동이 수출입과 무역수지에 미치는 영향

환율 변동이 수출입과 무역수지에 미치는 영향■ 원화가치의 하락은 단기적으로는 수입금액이 감소하면서, 중기적으로는 수출금액이 확대되면서 무역수지 적자폭을 축소하는 것으로 분석됨. - 국제무역이 주로 달러화로 결제됨에 따라, 단기적으로는 원화가치 하락이 수출물량에 미치는 영향은 크지 않은 반면, 수입가격(원화 기준)의 상승으로 수입물량은 큰 폭으로 축소되는 것으로 분석됨. - 중기적으로는 가격이 점진적으로 조정되면서 원화가치 하락이 수출물량에 미치는 영향이 점차 확대되는 것으로 나타남. ■ 최근의 글로벌 달러화 강세는 단기적으로 무역수지 적자를 유발하고 있으나, 원/달러 환율 상승이 무역수지 적자를 일부 완화하는 데 기여한 것으로 분석됨. - 올해 2/4~3/4분기의 글로벌 달러화 강세는 전반적인 교역을 위축시킨 가운데, 동 기간에 한국의 무역수지 적자를 60억달러 확대하는 요인으로 작용함. - 한편, 원/달러 환율 상승은 동 기간의 무역수지 적자폭을 20억달러 완화하는 데 기여한 것으로 분석됨. - 원/달러 환율 상승에 따른 가격조정의 영향이 점진적으로 나타나며, 최근의 글로벌 달러화 강세는 향후 2년 동안 무역수지 적자폭을 총 68억달러 축소할 것으로 분석됨. ■ 환율 변동은 다양한 경로를 통해 경제에 영향을 미칠 수 있으며, 본고의 분석 결과는 환율 변동이 무역수지 불균형을 완화하는 역할을 수행하고 있음을 상기함. - 각국의 거시경제 여건에 부합하는 통화정책은 환율 변동을 야기하면서 국가 간의 불균형을 완화하는 기제로 작용할 수 있음. - 따라서 외환시장이 원활하게 작동하는 한, 환율이 외환시장의 수급 여건에 맞게 자율적으로 결정되도록 용인할 필요 ■ 거시경제 안정을 위한 정책과 함께 환율 급등에 따른 수입물가 상승으로 어려움을 겪고 있는 취약계층 보호를 위한 정책도 병행할 필요 - 인플레이션이 높게 유지되는 가운데, 석유류와 전기, 가스 요금 등 수입물가에 밀접하게 연동된 품목의 가격상승은 취약계층의 부담을 가중할 가능성 - 광범위한 지원은 물가상승세를 억제하는 정책 기조와 상충될 수 있는바, 취약계층을 선별 지원하는 방안을 모색할 필요 ■ 중장기적으로 환율의 거시경제 안정 효과를 높이기 위해 국제상품 교역에서 원화거래 활성화를 위한 환경을 조성할 필요 - 국제교역이 대부분 달러화로 결제되는 경우 환율 변동의 수출에 대한 단기적인 영향이 미미하여, 무역 불균형 조정이 제한됨. - 중장기적으로 거시건전성 강화와 금융 및 외환시장 제도 개선 등을 통해 국제교역에 원화 사용이 활성화되기 위한 기반을 마련할 필요

-

김준형 동향총괄

프로필

프로필

-

한국개발연구원의 본 저작물은 “공공누리 제1유형 : 출처표시” 조건에 따라 이용할 수 있습니다. 저작권정책 참조

무단등록 및 수집 방지를 위해 아래 보안문자를 입력해 주세요.

담당자 정보를 확인해 주세요. 044-550-5454

소중한 의견 감사드립니다.

잠시 후 다시 시도해주세요.