Economic Outlook KDI Economic Outlook 2026-1st Half May 13, 2026

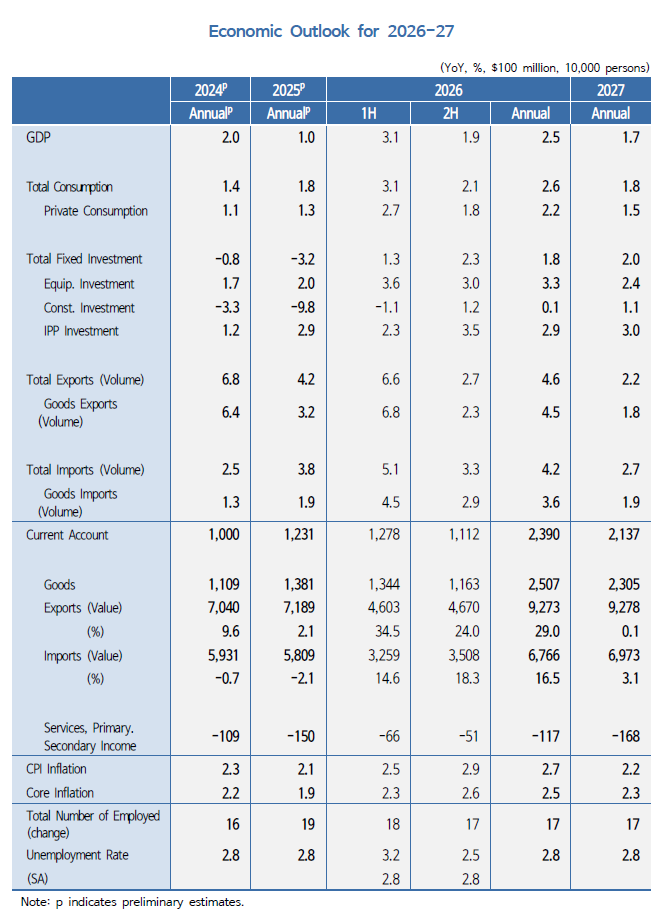

The Korean economy is projected to grow by around 2.5% in 2026, supported by robust semiconductor exports and a recovery in domestic demand, with growth expected at about 1.7% in 2027.

- Headline inflation is forecast to rise to around 2.7% in 2026, as higher international oil prices coincide with a recovery in economic activity, before moderating to about 2.2% in 2027 as oil prices decline.

- Despite demographic headwinds, employment is expected to continue improving gradually, with the number of employed persons increasing by 170,000 in both 2026 and 2027 as domestic demand recovers.

Ⅰ. Current Economic Conditions

- □ The Korean economy continues to recover, with growth gaining momentum amid strength in semiconductors and expanding domestic demand.

- · GDP increased by 1.7% quarter-on-quarter in the first quarter, led by semiconductor-driven export strength, while year-on-year growth rose to 3.6%, up from 1.6% in the previous quarter.

- · By sector, services improved, manufacturing rebounded, and the downturn in construction eased.

- □ Domestic demand has continued to recover alongside improving income conditions, but downside risks have increased amid the war in the Middle East.

- · Consumption continued to recover, while equipment investment improved, led by the semiconductor sector, and the contraction in construction investment moderated.

- · However, the rise in oil prices triggered by the war in the Middle East has pushed up production costs rapidly, while the Composite Consumer Sentiment Index fell sharply in April.

- · Inflation, which had been stable around the target, edged higher, and market interest rates also moved up.

- □ Exports continued to grow at a strong pace, supported by favorable semiconductor conditions despite a deterioration in the trade environment following U.S. tariff increases.

- · Export growth accelerated markedly, led by ICT products.

- · The current account surplus widened sharply, led by the goods account, as the terms of trade rose sharply on a surge in semiconductor prices and export volumes increased significantly.

- · With export growth and the improvement in the terms of trade sustained, the current account has remained in large surplus.

- □ Externally, uncertainty surrounding the war in the Middle East remains elevated and global growth is expected to moderate somewhat, although the semiconductor cycle is likely to remain favorable.

- · International oil prices have remained high despite sharp fluctuations, and the IMF recently projected a modest decline in global growth reflecting the war in the Middle East.

- · Consumer price inflation in major economies is rising rapidly, while the U.S. policy rate is expected to remain somewhat elevated.

- · At the same time, strong demand for memory semiconductors, which has underpinned the recent export expansion, is expected to persist for a considerable period.

Ⅱ. Domestic Economic Outlook for 2026-27

1. Key External Assumptions

- □ Global growth in 2026–27 is assumed to weaken somewhat under the impact of the war in the Middle East.

- · Reflecting the adverse effects of the war in the Middle East, the IMF recently projected global growth at 3.1% in 2026 and 3.2% in 2027, below the 3.4% recorded in 2025.

- □ Korea’s crude oil import price (Dubai) is assumed to stand at $91 per barrel in 2026, up from $69 in 2025 due to the war in the Middle East, before declining to $82 in 2027.

- □ The Korean won’s real effective exchange rate is assumed to remain broadly stable at its recent level.

2. Domestic Economic Outlook

- □ The Korean economy is projected to grow by around 2.5% in 2026, supported by robust semiconductor exports and a recovery in domestic demand, with growth expected at about 1.7% in 2027.

- · Growth is expected to run above potential in 2026–27, leaving the economy in an expansionary phase.

- · Private consumption is projected to recover, rising by around 2.2% in 2026 and 1.5% in 2027, supported by improving income conditions and government support measures despite the inflationary impact of the war in the Middle East.

- · Equipment investment is expected to expand by around 3.3% in 2026 and 2.4% in 2027, supported by robust investment demand from the semiconductor upturn despite weakness in non-semiconductor sectors.

- · Construction investment is projected to increase only marginally in 2026, by 0.1%, as higher construction costs stemming from the war in the Middle East delay its recovery, before growth rises to around 1.1% in 2027.

- · Exports are expected to increase by around 4.6% in 2026, supported by the semiconductor upcycle, and to maintain solid growth of around 2.2% in 2027.

- · The current account is projected to post a particularly large surplus, driven by a sharp increase in semiconductor exports.

- □ Headline inflation is forecast to rise to around 2.7% in 2026, as higher international oil prices coincide with the recovery in economic activity, before moderating to about 2.2% in 2027 as oil prices decline.

- □ Despite demographic headwinds, employment is expected to continue improving gradually, with the number of employed persons increasing by 170,000 in both 2026 and 2027 as domestic demand recovers.

3. Risks to the Outlook

- □ Growth could strengthen further if semiconductor supply capacity expands rapidly.

- ·Given the surge in semiconductor demand, an increase in semiconductor supply capacity could lift real GDP growth, which is measured in volume terms.

- □ Growth could weaken if the war in the Middle East escalates or becomes prolonged, as disruptions to commodity supply and higher production costs weigh on activity.

- · Considerable uncertainty surrounds the course of the war in the Middle East, and a prolonged blockade of the Strait of Hormuz could push up production costs across the broader economy.

Ⅲ. Policy Directions

1. Monetary policy

- □ Monetary policy should respond flexibly to the risk that inflation expectations could become destabilized amid improving economic activity and a sharp rise in international oil prices.

- · Demand-side inflationary pressures are building as private consumption improves, while higher international oil prices have added substantially to supply-side pressures.

- · Monetary policy therefore needs to guard against destabilized inflation expectations, while taking domestic and external uncertainties into account.

2. Fiscal policy

- □ Fiscal policy should focus spending on raising potential growth and supporting income-vulnerable groups, while continuing efforts to improve spending efficiency.

- · Under the National Fiscal Management Plan for 2025–29, basic pension spending and local education finance grants are expected to exceed 100 trillion won next year, underscoring the need to actively pursue spending-efficiency reforms, including for mandatory expenditures that require legislative amendments.

- · In particular, basic pension support should be targeted more closely to vulnerable older persons, while local education finance grants should be restructured to reflect the school-age population.

Analysis of current economic issues

-

-

Changseok Ma

profile

profile

-

-

-

Changseok Ma

profile

-

We reject unauthorized collection of email addresses posted on our website by using email address collecting programs or other technical devices. To access the email address, please type in the characters exactly as they appear in the box below.

Please enter the security code to prevent unauthorized information collection.